By Keith Gangl

The stock market, represented by the S&P 500, entered March in positive territory, but that changed quickly. Investors experienced a sharp pullback, what might aptly be called the “March Slide.”

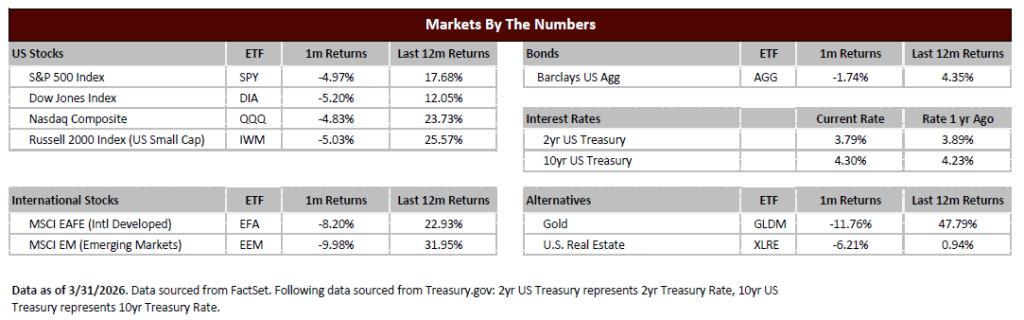

The S&P 500 fell 4.97% during the month, dragging both quarterly and year-to-date performance into the red, with a decline of 4.63%[1], through the first three months of the year.

Markets sold off largely due to the escalating US/Israel conflict with Iran. Investors have little tolerance for geopolitical uncertainty, and the turmoil in the Middle East has injected significant anxiety into financial markets.

Compounding that uncertainty, there has been a dramatic surge in oil prices — rising from approximately $67 per barrel at the beginning of the month to over $100[2] by month’s end. This kind of spike acts as a de facto tax on the broader economy, creating headwinds for consumers and businesses alike.

In the near term, corporate fundamentals have not yet deteriorated, but there is a growing fear that it may only be a matter of time before elevated oil prices begin to weigh on both the US and global economies. This anxiety, in part, explains the market’s difficult March.

With no clear consensus on how long oil prices will remain elevated, or at what level, volatility and uncertainty are likely to persist.

It is worth noting that if conditions in the Middle East shift, which geopolitical situations often do, and sometimes quickly, the primary headwind facing the market could ease considerably. That would allow investors to refocus on company fundamentals, which have remained broadly solid throughout this period of turbulence.

The current selloff carries echoes of last year’s sharp market decline following “Liberation Day,” which was the announcement of sweeping new tariffs by President Trump. At the time, investors reacted with fear and uncertainty, selling off nearly 20% in a matter of weeks.

That selloff ultimately proved to be a buying opportunity: the market subsequently surged 38%, finishing 2025 up over 17%[3] for the year. History may not repeat itself exactly, but the pattern of fear-driven selloffs followed by recovery is one that investors would do well to keep in mind as they assess the current environment.

Markets have always faced uncertainty; this year is no different, and in some respects the concerns may be more pronounced than in a typical year. Yet over time, markets have consistently demonstrated the ability to overcome adversity and grind higher.

In uncertain moments like these, it is essential for investors to remain disciplined, stay focused on company fundamentals, and resist the temptation to make emotional decisions based on short-term noise.

One of the most important lessons from both last year’s tariff-driven selloff and the current conflict-driven decline is this: uncertainty is temporary, but the long-term trajectory of well-managed businesses is not.

For patient investors, periods of market stress have historically represented not just a risk to manage, but an opportunity to seize. While no one can predict how the conflict in the Middle East will unfold or where oil prices will settle, investors who stay grounded in fundamentals, maintain their discipline, have a diversified plan, and resist the pull of fear are best positioned to benefit when clarity, as it inevitably does, returns to the market.

[1] S&P 500 Returns

[2] March Oil Prices

[3] FactSet: S&P 500 Returns