By Tyler Ellegard, CFA®

The U.S. dollar has long been the cornerstone of the global financial system — the world’s primary reserve currency, accounting for roughly 58%1 of global reserves, and the denomination of choice for commodities, cross-border loans, and international trade. Yet every few years, typically in the wake of a geopolitical shock, the same question resurfaces: how much longer can the dollar hold the throne?

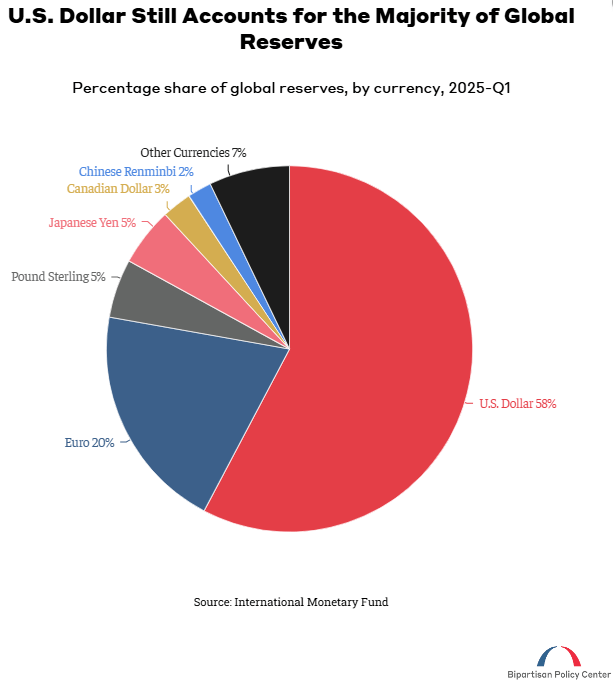

The numbers paint a remarkably durable picture, as shown in the pie chart above.2 As of early 2025, the dollar still accounts for 58% of global foreign exchange reserves, which is more than the next six currencies combined. Its closest rival, the Euro, sits at just 20%, while the Japanese Yen, British Pound, and Chinese Renminbi each hold modest single-digit shares. And reserve holdings are only part of the story as the dollar is present in nearly 89%1 of all global foreign exchange market transactions, a reflection of just how deeply embedded it is in the plumbing of international finance. For all the headlines about rising challengers, no currency has come close to mounting a serious threat to the dollar’s commanding lead.

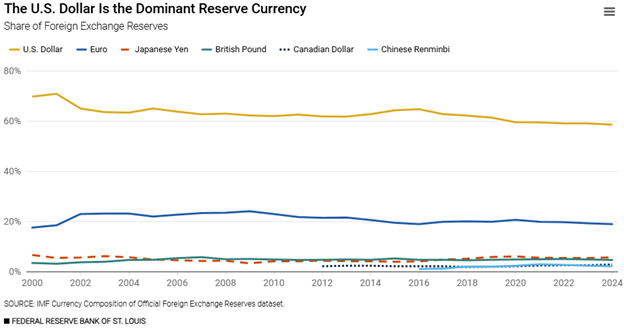

Zoom out over the past two decades, and the story becomes even more interesting. Yes, the dollar’s share of global reserves has drifted down from nearly 70% in the early 2000s to around 58% today, as shown in the graph above3, however, context matters. Much of that diversification happened during periods when the dollar strengthened aggressively, most notably in the post-pandemic era when the Fed’s rapid rate hikes sent the dollar surging. Foreign central banks naturally rebalanced, trimming dollar holdings not out of distrust, but out of basic portfolio management. What’s striking is how little ground the dollar actually lost despite those headwinds. No single currency stepped in to absorb the shift; reserves simply spread across a broader basket. That isn’t a story of dethroning. It’s a story of diversification at the margins, with the dollar holding firm at the center.

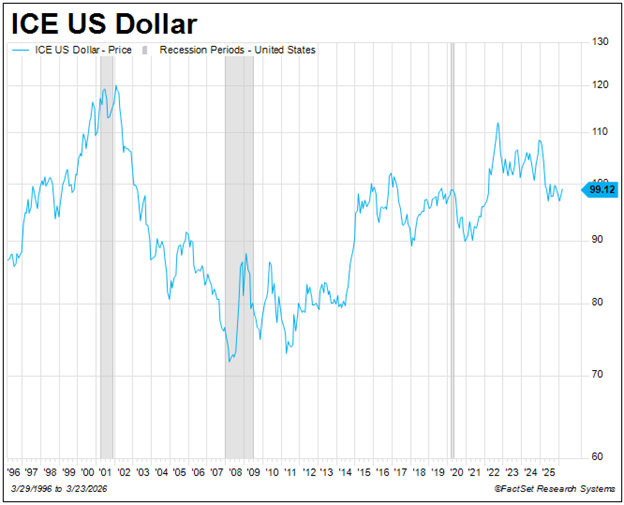

Perhaps the most visible challenge to dollar dominance has come from the BRICS nations, a bloc that has expanded in recent years and now represents a significant share of global GDP. The group has been vocal about reducing dollar reliance, yet the practical obstacles remain steep — a credible reserve currency requires deep and liquid financial markets, rule of law, and political stability, qualities the BRICS bloc has struggled to offer collectively. The desire to diversify is real; the ability to execute it at scale is another matter entirely. The ICE U.S. Dollar Index, which measures the dollar against a basket of major world currencies, reinforces this point. Despite surging to multi-decade highs in 2022 and prompting some central banks to rebalance their reserves, the index today hovers near 994, well within its long-term range and hardly the portrait of a currency loosening its grip on the world.

For investors, the dollar’s gradual evolution is less a warning signal and more a reminder to think globally. A structurally softer dollar over the long term tends to create tailwinds for international equities, commodities, and real assets and a world that rewards investors who are diversified across those asset classes. The dollar will almost certainly remain the world’s dominant reserve currency for decades to come. But dominant doesn’t mean static, and investors who understand that distinction are better positioned for whatever the next chapter brings.

1. iiss.org/online-analysis/six-analytic-blog/2026/01/the-future-of-dollar-dominance/

2. https://bipartisanpolicy.org/explainer/whats-behind-the-u-s-dollars-dominance-and-why-it-matters/

3. https://www.stlouisfed.org/open-vault/2026/feb/us-dollar-role-as-reserve-currency

4. FactSet Research Systems